Last year was a tumultuous one for mortgages, none more so than after then Prime Minister Liz Truss' mini-budget in September.

While mortgage rates were already gradually rising due to high inflation, the surprise list of unfunded tax cuts caused costs to skyrocket.

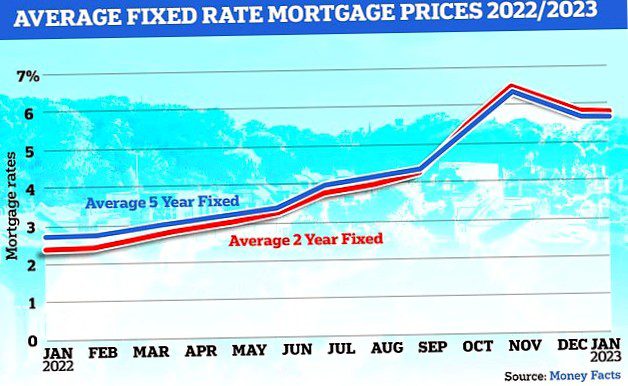

On 1. August 2022, the average interest rate on two-year fixed-rate mortgages across all deposit sizes was 2.52 percent, according to Moneyfacts data.

The number reached 20. October peaked at 6.65 percent, with the five-year fixed rate at 6.51 percent on the same day.

However, average fixed rates for two- and five-year mortgages have been falling steadily, despite a series of prime rate increases by the Bank of England to counter high inflation. They now stand at 5.78 percent respectively. 5.62 percent.

We look at whether mortgage rates will continue to fall this year and what borrowers need to know.

Mortgage rates rose rapidly last year after the disastrous "mini-budget" in September

For those in need of a mortgage, the cost increase has been significant in recent months.

First-time buyers may find it harder to get a mortgage approved as higher interest rates, combined with the cost of living crisis and higher rents, put additional pressure on household finances.

In the meantime, homeowners who are at the end of a fixed-term contract are likely to face higher mortgage rates, which could add hundreds of pounds to their monthly payments.

>> See how much a higher mortgage rate would add to your monthly payments

What's going to happen to mortgage rates this year?

Most experts now expect average mortgage rates to settle between 4 and 5 percent this year. This is based on their assumption that inflation has peaked and as a result the Bank of England will slow its prime rate increases.

Although only tracker mortgage rates are directly affected by the prime rate, increases are often passed on by lenders to customers, affecting the overall cost of borrowing.

There are also signs that the housing market is cooling, which could lower mortgage rates as lenders will compete for customers.

Changing times: volatility in the mortgage and real estate market has unsettled borrowers

Should people put off buying a home or relocating?

With the cost of fixed-rate mortgages slowly falling, those thinking of moving or buying, or needing to restructure their debt, may be tempted to leave it as long as possible to potentially benefit from lower rates.

Interest rates have fallen steadily from the last quarter of 2022 into the new year. Am 1. November 2022, the average interest rate for two-year fixed-rate mortgages was 6.47 percent and is now 5.78 percent.

That means someone taking out a new mortgage today for 200.£000 lock would typically pay £85 less a month than someone who locks in November.

Interest rate outlook: Brokers expect mortgage rates to level off between 4% and 5% in 2023

In uncertain times, Vicki Harris, chief commercial officer at Kensington Mortgages, says it's important borrowers get the right advice. This, she says, means consulting a broker who can survey the entire market and find the best deal for your personal circumstances.

Use our mortgage finder tool to search for the latest mortgage rates and get free advice from L&C, This is Money's broker partner.

"Advice is vital as an increasing number of borrowers may not meet the lending criteria of high-street banks and therefore may need to consider some of the more specialist options in the market," says Harris.

"If you think home prices are likely to fall in the coming months, it may make sense to wait and see how the market evolves before making big financial decisions."

It may also be worth exploring more flexible options to take advantage of lower interest rates. In low interest rate environments, such as those seen over the past two years when rates fell to 0.1 per cent, it would not be worth getting a tracker rate as they are unlikely to fall.

However, many tracker interest rates are currently cheaper than fixed contracts and could be a way to save money, at least for borrowers who are comfortable with the idea of changing monthly payments.

The average two-year tracker rate is about 5.5 percent and the five-year is about 5.25 percent.

Borrowers should contact a broker and find out if they can reschedule without penalties if fixed rates become cheaper than their pursuer.

Will 5% and 10% mortgages still be available?

As household finances continue to come under pressure, there are fears that lenders will reduce the number of low deposit mortgages on offer and make their affordability criteria stricter.

This happened at the beginning of the Covid pandemic, when banks were worried about the extent of potential job losses.

Redrow's James Holmear says mortgage lenders are still keen to do business

However, experts say many lenders will have already factored higher inflation into their affordability calculations.

In addition, the government has announced a one-year extension of its mortgage guarantee program, where it will guarantee 95 percent of loans to encourage banks to originate them.

James Holmear, group sales director at housebuilder Redrow, says: "While interest rates and the general cost of living can put pressure on borrowers' ability to borrow, the appetite for banks to do new business is still incredibly strong."

What should you do if you need to reschedule your debt?

Half of UK homeowners have a fixed rate mortgage that expires within the next two years. While interest rates are now falling from their autumn highs, many of these borrowers are still likely to see their monthly payments rise significantly – at a time when incomes are already strained.

The FCA recently issued guidance for mortgage lenders on supporting borrowers affected by the rising cost of living.

So what can you do if you need a new mortgage?

Early preparation is key, says Chris Sykes, technical director at mortgage broker Private Finance.

"Lenders will often let you agree on a new interest rate months before your current contract expires, and some have extended the window to six months before your current contract ends, rather than three," he says. "If rates improve towards the end of your current deal, you can switch again, but it protects you if they go up," he says.

First-time buyers may be reluctant to take the leap, but experts say it's still a good investment

It's also important to make sure you have the right broker with access to as many lenders as possible to ensure you get the best deal.

>> What to do if you're struggling to afford your mortgage payments

Brokers can also save you time by making sure you don't apply for a mortgage you don't qualify for.

You will receive advance notice of changing interest rates and can access "broker-only" offers that are not available when you contact a lender directly.

What first-time buyers should think about?

If you are an aspiring first-time buyer and have been discouraged by developments in the property market such as increased rates and the end of Help to Buy, it's important to remember that there are still options available to you.

More than ever, it's important for first-time buyers to get the basics right, Coulson says.

There are a growing number of mortgage products available, and a clear understanding of your options as well as your likely borrowing capacity puts you in the best position to bid on properties from a strong position.

"You need someone to just give you some home truths, and a broker does that and does it brilliantly," adds Jon Cooper, head of mortgage sales at Aldermore Bank. It's also worth asking what flexibility lenders have to accommodate your financial circumstances.

"At Aldermore, we can look at 40-year maturities and have always been able to consider multiple income streams for applicants as long as they are plausibly sustainable – both of which can be helpful from an affordability perspective.

"If a borrower needs to seek help and support for a larger deposit at the Bank of Mum and Dad, we're also happy to accept a fully gifted deposit from a close relative," he adds.

What to do if you need a mortgage?

Borrowers who need to find a mortgage because their current fixed rate deal is expiring or because they have agreed to buy a home should explore their options as soon as possible.

This is Money's best mortgage rate calculator, backed by L&C, and can show you quotes that match your mortgage and property value

What if I need to restructure my debt?

Borrowers should compare interest rates and speak with a mortgage broker and be prepared to trade to secure an interest rate.

Anyone with a fixed-rate deal that ends within the next six to nine months should check how much it would cost them to reschedule now – and consider taking out a new deal.

With most mortgage transactions, fees can be added to the loan, which are then only calculated at closing. This way, borrowers can secure an interest rate without having to pay expensive brokerage fees.

What if I'm buying a home?

Those who have agreed to buy a home should also aim to secure installments as soon as possible so they know exactly how much their monthly payments will be.

Homebuyers should be wary of overextending themselves and be prepared for the possibility that home prices could fall from their current high levels as higher mortgage rates limit people's borrowing ability.

How to compare mortgage costs

The best way to compare mortgage costs and find the right deal for you is to talk to a good broker.

You can use our best mortgage rates calculator to view quotes that match your home value, mortgage size, term and fixed rate needs.

However, please note that interest rates can change quickly. So if you need a mortgage, you should compare interest rates and then talk to a broker as soon as possible so they can help you find the right mortgage for you.